Channelling the rising pool of African capital – through native and regional funds, banks, ECAs and DFIs – into African infrastructure at scale has each logical argument going for it. From mitigating foreign exchange dangers to deepening capital markets, rising the native pool of funding will present a mess of advantages. Moreover, poor infrastructure reportedly provides 30-40% to the prices of products traded amongst African international locations, in addition to a plethora of different hardships.

However the logic ignores a number of the realities of the potential African funding base. Based on Samuel Chasia, director of enterprise growth – capital markets at GuarantCo (a part of the PIDG Group), this prospect faces two massive points: “What is really a hindrance to getting financing into infrastructure tasks is capability and, in numerous monetary establishments, urge for food. The mixture of those two issues is detrimental”.

A big impediment is financial savings (or the shortage of). Compared to different rising economies with related populations and GDPs, financial savings charges are very low throughout Africa – in line with the Africa Monetary Business Summit, solely 15% of Africans have pension protection, far beneath the worldwide common of 54%. Extending protection to the 80% of the workforce within the casual sector poses an extra mammoth process.

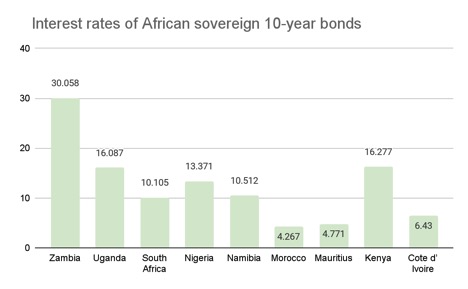

The second situation is the excessive price of presidency borrowing: of the 9 African sovereigns at present issuing ten-year bonds, the benchmarks vary between 426bp and 3005bp (depicted within the graph beneath). As Ope Onibokun, funding director for infrastructure & local weather at BII, says “When you can earn 20% borrowing from the federal government, which is taken into account risk-free, investing in infrastructure might be comparatively unattractive if the anticipated returns don’t stake up”.

Supply: Investing.com

Supply: Investing.com

Elena Palei, world head of infrastructure at MIGA, soundly encapsulates the fact, “large-scale African infrastructure tasks couldn’t rely 100% on home liquidity.” Small ticket regionally funded offers may also help to shut the infrastructure hole – however provided that a plethora of such offers are realised.

Institutional funding routes

In March 2022, IFC signed a $10 million partnership with Senegal’s sovereign wealth fund (SWF), Le Fonds Souverain d’Investissements Strategiques (FONSIS), to develop 200 houses in Dakar over the subsequent eight to 10 years. The small-ticket deal may also help scale up influence and can mobilise further native and worldwide institutional funding.

SWF sizes may enhance with hikes in commodity costs – however this won’t be as probably as hoped. Nigeria Sovereign Funding Authority (NSIA) receives extra money from crude oil with barrel costs growing to $18 every previously 12 months – however pipeline closure and constrained manufacturing has led the nation’s oil output to new lows. Conversely, persevering with political unrest and underinvestment will proceed to restrict SWF inflows, which already wrestle to make an impactful capital dent: the continent’s SWFs solely noticed incomes of $130 billion during the last 5 years (2016-2020).

In Kenya, Nigeria, and South Africa, pension and insurance coverage represents a barely extra important pool of liquidity, with AUMs of $12.2 billion, $30.2 billion, and $302.1 billion, respectively (2021). Equally to SWFs, these sources match the character necessities of infrastructure funding: they’ve a long-term view and can profit from infrastructure money flows which permit them to satisfy obligations like premium pay-outs. Briefly, educating institutional traders about funding infrastructure is vital to making sure their transfer away from authorities treasuries.

Nevertheless, threat isn’t just as a matter of returns, as Onibokun highlights: “it’s important to satisfy the money expectations of coverage holders – you’ll be able to’t count on pensioners to come back to the tip of their coverage and discover on the market’s no cash”. Any capability gaps in infrastructure experience should be addressed completely earlier than encouraging funding – TA, consultancy recommendation, and assure constructions may soften this threat.

Each swimming pools lack the liquidity and capability crucial for scaled up infrastructure funding – however mixing these sources collectively, as Africa50 has efficiently managed to do with the Africa50 Infrastructure Acceleration Fund, in a approach resolves each limitations.

The $500 million fund was signed in July 2023 and secured subscription agreements from NSIA, IFC, AfDB the Arab Financial institution for Financial Improvement in Africa (BADEA), BOAD, CDC Senegal, CDC Benin, CNSS Togo, CDG Make investments, and Attijariwafa Financial institution of Morocco, in addition to pension funds, asset managers, retirement businesses and two worldwide institutional traders. It marks the primary personal car infrastructure platform launched by the agency and an “unprecedented milestone for Africa”, in line with AfDB, which invested $20 million of fairness into the fund.

It’s nonetheless unclear whether or not the fund will harness one of many best property of home mobilisation: native foreign money financing. Except for the development of the Malicounda energy station in Senegal which price Africa50 and Oragroup XOF50 billion ($90 million) in March 2021, the agency has tended to favour {dollars} and euros. Not doing so dangers slicing additional into the already restricted home financial savings swimming pools with foreign exchange threat changes.

“Probably the most environment friendly solution to finance these infrastructure tasks is with native foreign money in any other case you’re introducing foreign money mismatches which is a value that finally anyone has to bear” says Chasia, “When you’re financing one thing for 15-20 years, any mismatches will finally influence the affordability and sustainability of the undertaking.”

Native foreign money routes

DFI ensures can finance native foreign money tasks with home involvement and GuarantCo has a confirmed observe file: The DFI supplied a XAF23.5 billion ($38.4 million) assure answer to Societe Generale Cameroun and Societe Commerciale de Banque Cameroun (SCB) to finance the modernisation of 14 toll plazas throughout Cameroon in June 2022. The financing includes a 14-year mixed liquidity extension and partial credit score assure to help the debt and lend consolation to the 2 banks mixed mortgage of XAF32.2 billion ($52.5 million). Six months later, GuarantCo and African Assure Fund (AGF) supplied GreenYellow with a nine-year credit score assure of MGA 23.5 billion ($5.4 million) to a syndicate of native banks, led by Societe Generale, to finance a 20MW photo voltaic plant extension alongside a 5MW photo voltaic battery storage system in Madagascar.

Each tasks managed to unlock regionally sourced, native foreign money financing on appropriate tenors to undertaking financing. The bones of sustainable structuration are there – however ensures are nonetheless hesitant to tackle bigger tickets or building threat.

Public debt markets pose an alternative choice for native foreign money financing and twenty inexperienced bonds have been floated in Africa since 2020, elevating a complete of $2.78 billion. As highlighted above, bonds are engaging to traders for his or her capability to ship dependable, excessive returns – channelling that revenue into infrastructure appears a easy answer.

In October 2019, GuarantCo supplied a 50% partial credit score assure to traders in Acorn Holding’s KES 4.3 billion ($43 million equal) notice programme, overlaying principal and curiosity on account of fund the development of lodging for five,000 college students in Nairobi. The bond was priced at 12.25% and was rated B1 by Moody’s (greater than the sovereign bond score).

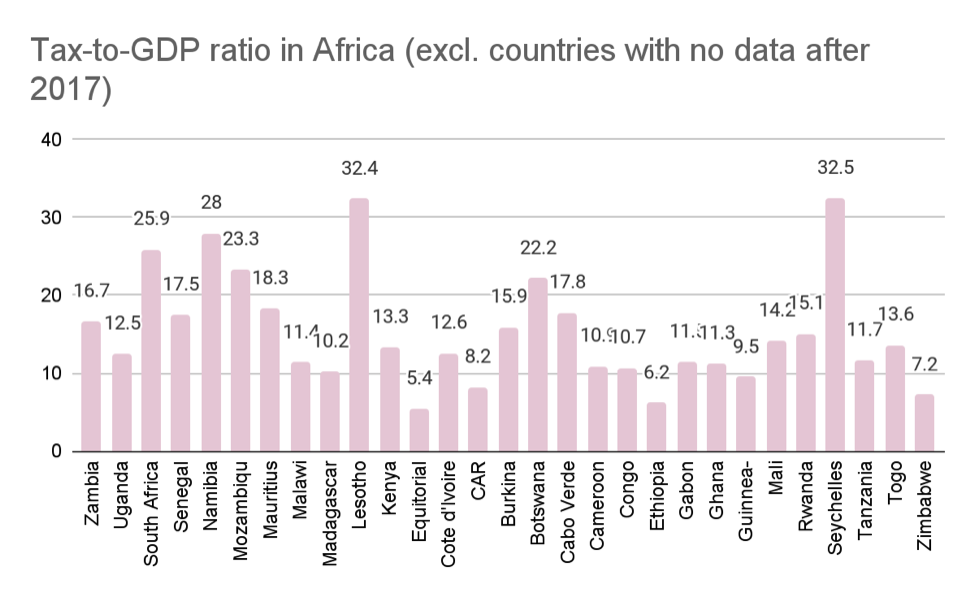

Past GuarantCo’s progressive deal, nonetheless, the continent’s public debt markets are invariably thinly traded and dominated by authorities points, which raises a difficulty for protecting a lid on sovereign debt. African international locations have a mean 70% debt-to-GDP ratio which is beneath the worldwide imply however not the worst – however the higher situation arises whenever you come to tax-to-GDP ratios. As seen within the graph beneath, for some sovereigns already dealing with debt sustainability points (like Ghana, Zambia, Ethiopia, Gabon) scaling up bonds may make debt unserviceable.

Supply: World Financial institution

On the company facet, undertaking finance requires massive sums to be drawn down firstly for building, the riskiest section of the enterprise. Personal traders could also be inquisitive about money flows from maturer infrastructure however these bonds are nearly solely absent from the continent.

The primary itemizing of an investment-grade rated infrastructure undertaking bond came about in April 2013 in South Africa, with institutional traders solely backing the 44MW Touwsrivier Photo voltaic Venture with a hard and fast coupon of 11% over a 15-year maturity date. Regardless of the innovation of the issuance, which was primarily based on an amortising profile rather than a bullet construction successfully giving the bond a modified length of seven years, the South African market hasn’t seen many subsequent undertaking bonds – and so they have been lacking solely from different African markets.

DFI-ECA cooperation routes

As outlined already, DFIs are a big participant on the African infrastructure panorama: in line with Uxolo information, between 2021-2023 DFIs have invested $11.46 billion on this house (together with closed and permitted offers). Blended finance first-loss buffers are a standard technique for DFIs to guard pure play personal capital traders, together with native ones.

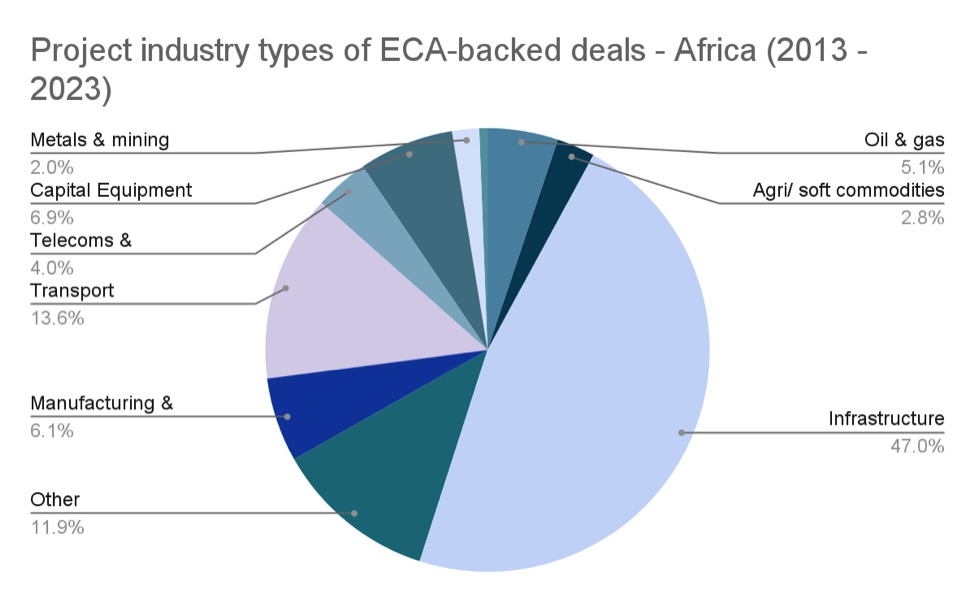

However DFIs will not be the one company financiers current on the continent: ECAs have been actively mobilising billions in worldwide and native (primarily South African) industrial capital into infrastructure which, within the final decade, has made up 47% of African offers (in line with TXF information, chart beneath). General, ECA undertaking volumes have eclipsed DFI’s: of the 68 ECA-backed infrastructure offers which have closed between 2021-2023 have amounted to $15.3 billion (TXF information).

Supply: TXF information

DFI-ECA collaborations now must step up for the sake of accelerating influence {dollars}: the ECA mandate reduces growth to a byproduct of transactions, not the objective, and DFIs can not obtain the SDGs solely on their very own, restricted, capital.

The DFIs which have been prepared to collaborate on ECA-backed offers have been African; particularly, AFC, AfDB, and Afreximbank. Western DFIs have been barked off by tensions round most popular creditor standing, like IFC on the $2.7 billion Nacala Logistic Hall in Southeast Africa.

With latest updates within the OECD Association on Formally Supported Export Credit being touted as a “nice milestone” for growing the local weather and influence targets of ECA finance flows – by (i) growing tenors to as much as 22 years for climate-focused tasks (from 18 beforehand); (ii) introducing additional reimbursement flexibility, and (iii) adjusting the minimal premium charges for credit score threat for longer reimbursement phrases and obligors with greater credit score threat rankings – the time has by no means been so ripe for DFI-ECA climate-aligned collaboration in more durable risk-climates. Underserved African infrastructure presents the right problem and alternative.

The TXF perspective

Bonds, blended finance, funds, SWFs, pensions, ECAs – combining native foreign money, capability and capital is proving a troublesome process throughout the board. The one financing supply that’s managing to ship all three reliably and repeatedly is ensures, however examples are nonetheless skinny on the bottom.

Ensures can enhance the bankability of particular tasks, however Palei says they nonetheless aren’t “the last word answer” and can’t substitute sector reforms – if the tariff system is insufficient, authorities owned utilities are weak, authorities establishments concerned within the regulation and supervision of tasks are insufficient, then these will all deter the event of a bankable undertaking pipeline.

Native foreign money is a preferable answer, however there are nonetheless circumstances the place it isn’t doable. MIGA can solely present ensures in convertible currencies and GuarantCo has to make allowances for laborious foreign money when crucial to take action, corresponding to in fragile economies. However, this inhibition could be much less vital than urged, as Chasia states that: “As an African myself, I desire extra capital within the area – there’s a necessity for every type of financing and, finally, having no important infrastructure is much more costly than having laborious foreign money debt”.

With Chasia’s phrases in thoughts, extra DFI-ECA collaboration turns into the obviously apparent choice for scaling up infrastructure capital.

{kind=link}